Each type of investment has its own set of characteristics and is suitable for different investor needs and risk tolerance levels. Diversifying across multiple types can help manage risk and improve the potential for returns, but it is important to understand the risk factors of each investment before entering any investment.

Understanding how money works is more than just numbers—it’s empowerment. A strong grasp of financial basics helps individuals make better decisions about spending, saving, and investing. In cities like Tyler and Dallas, where living costs can fluctuate, financial literacy gives people the tools to thrive, not just survive.

It also helps you spot risk, ask the right questions, and plan confidently for the future. With better knowledge, you can avoid debt traps, prepare for emergencies, and grow your wealth with purpose.

This is exactly what Plush Retirement is committed to—educating individuals and families across Texas through accessible, easy-to-understand guidance from experienced professionals like your trusted Financial Advisor or Personal finance advisor.

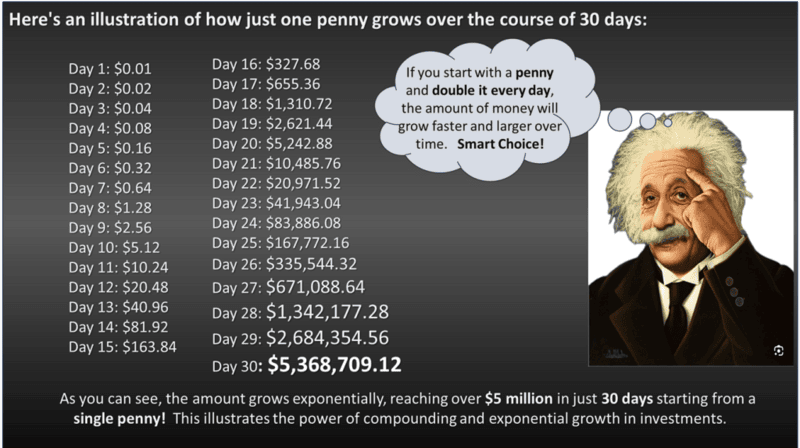

1.) One million dollars in silver

or

2.) One penny that you would double every day for a month (30 days) and keep all the change after day 30……

Which would you pick??

We hope for your future to be prosperous and trouble-free. See how our strategic planning services can protect a comfortable lifestyle in your retirement.