- If you lost 30% in the stock market last year, but then you gained 30% this year…..

- You are thrilled that you can trade a stock

- You are even

- You are ahead

- You are still at a loss

- It depends on your location

- If you have a 6% fixed ROI/Rate of Return. Approximately, how long should it take to double your investment?

- 6 years

- 9 years

- 10.2 years

- 12 years

- 15 years

- Tina is 45 years old, single, and makes $300,000 annually. How much can she contribute to her Traditional or Roth IRA per year for 2024 or 2025?

- None

- $5,000

- $6,000

- $7,000

- $22,000

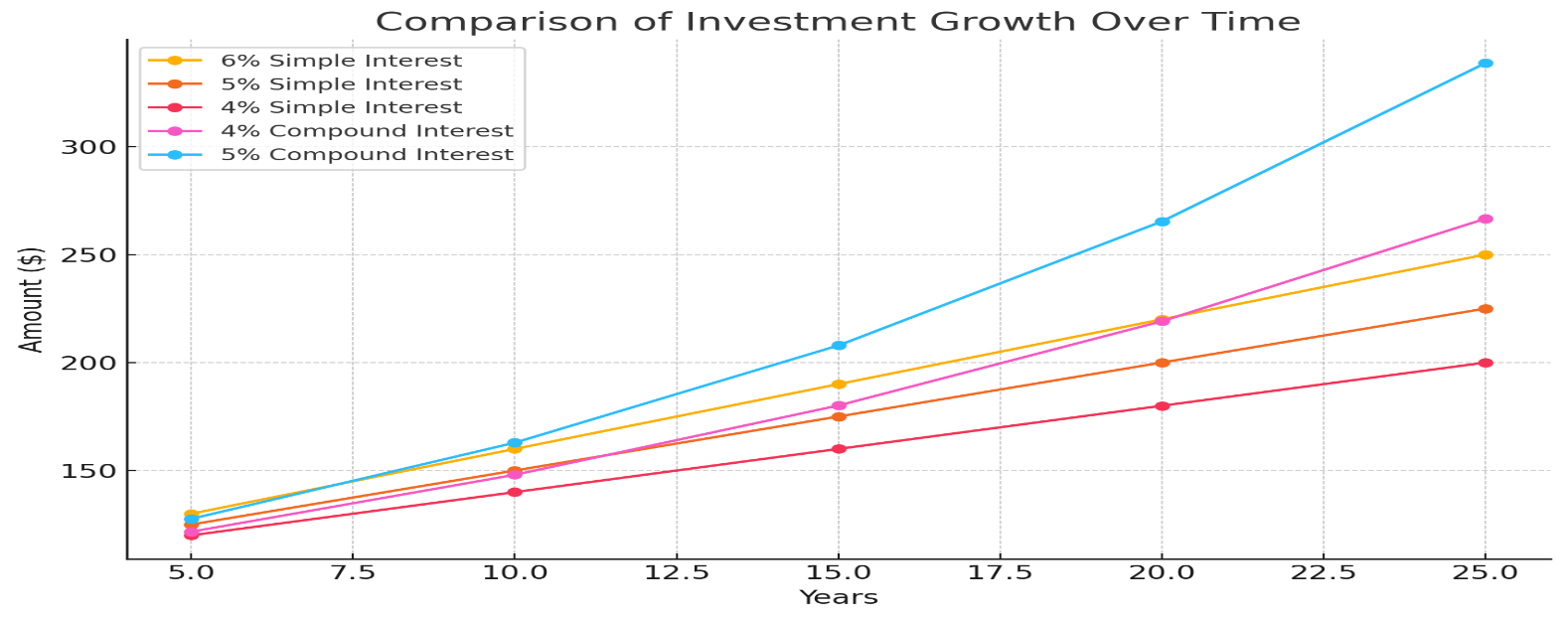

- Which would make more money in Ten Years

- 6% Simple Interest

- 5% Simple Interest

- 4% Simple Interest

- 4% Compound Interest

- 5% Compound Interest

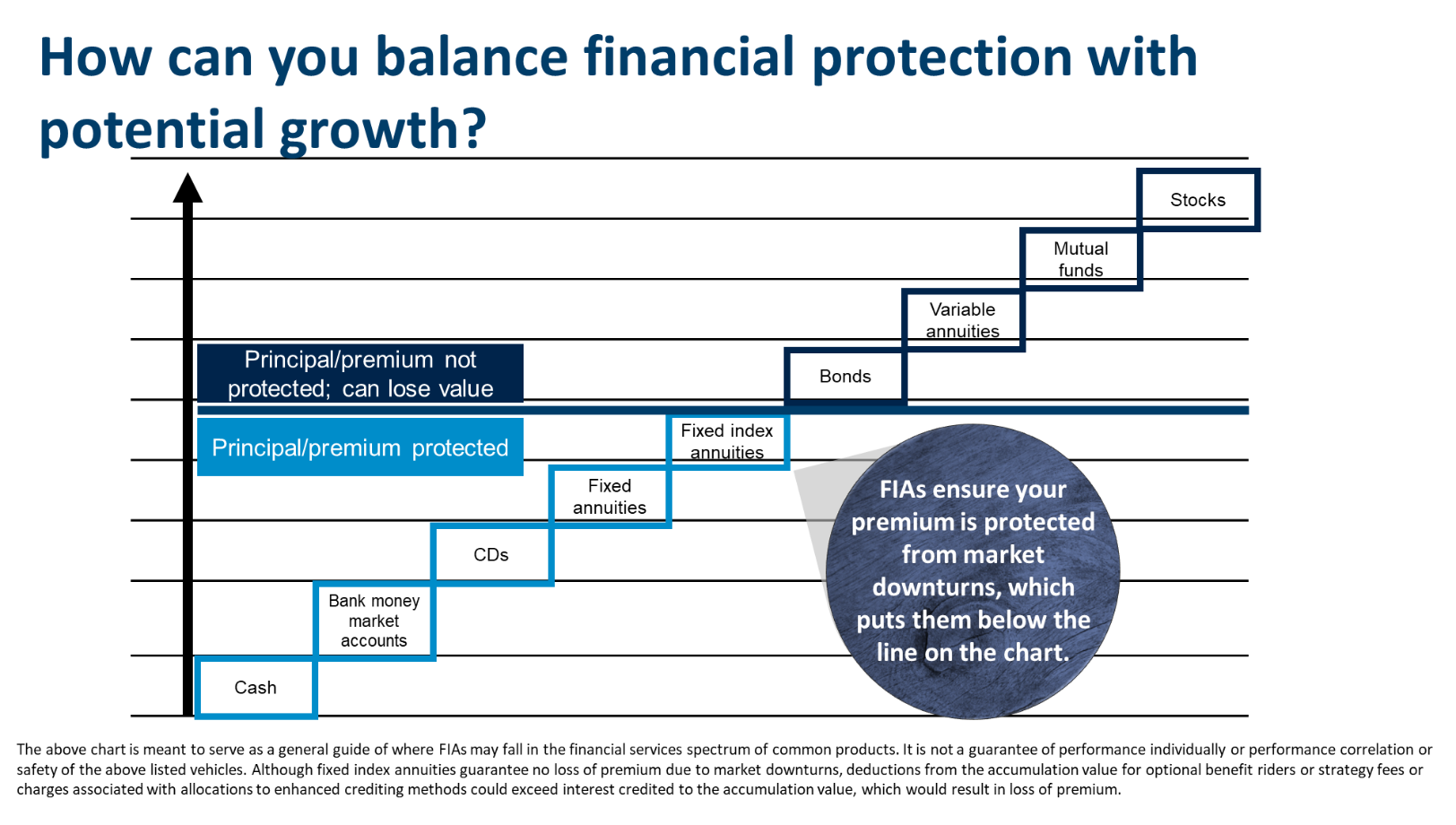

- Which of the following financial products and solutions are guaranteed to never lose any of your principal?

- Stocks /Mutual Funds / ETFs

- Variable Annuities

- Fixed-Indexed Annuities

- Bonds

- Bitcoin /Cryptocurrency

- Which would make more money in Five Years

- 6% Simple Interest

- 5% Simple Interest

- 4% Simple Interest

- 4% Compound Interest

- 5% Compound Interest

- In the event of a death in which a family is paid a death benefit of $100,000 on a life insurance policy, how much would they be taxed by the IRS?

- $22,000

- $12,000

- $0

- $10,000

- $18,000

- The average life expectancy of a man and woman (in 2023) is

- Man – 69 Woman – 75

- Man – 75 Woman – 80

- Man – 76 Woman – 79

- Man – 85 Woman – 89

- Man – 90 Woman – 94

- World Health Organization (WHO):

- The WHO provides comprehensive global health statistics, including morbidity and life expectancy data.

- Website: who.int

- Centers for Disease Control and Prevention (CDC) (for the United States):

- The CDC offers detailed health statistics, including life expectancy and morbidity data for different demographics.

- Website: cdc.gov

- National Center for Health Statistics (NCHS):

- A division of the CDC, the NCHS provides a wide range of health statistics, including life expectancy tables.

- Website: cdc.gov/nchs

- United Nations Department of Economic and Social Affairs (UN DESA):

- The UN DESA publishes global population and health statistics, including life expectancy.

- Website: un.org/development/desa

- OECD (Organization for Economic Co-operation and Development):

- The OECD provides health data for its member countries, including life expectancy and morbidity rates.

- Website: oecd.org

- National Institutes of Health (NIH) (for the United States):

- The NIH provides extensive research and statistics on various health conditions, including morbidity and mortality data.

- Website: nih.gov

- What are the chances of needing Long Term Care (Permanent Hospitalization) in your golden years?

- Below 30%

- 30% to 45%

- 46% to 60%

- 61% to 75%

- Above 75%

- How much do credit inquiries from creditors checking your credit worthiness by pulling your credit account for your credit score?

- 5%

- 10%

- 15%

- 20%

- 30%

The correct answer would be 5% Compounding Interest, since it is able to add each previous year’s gains to each annual gain. See the graph above. If only a few years then it might still be advantageous to take the higher interest rate, but the longer time span, the greater the compounding effect and even 4% compounding interest outpaces 6% simple interest at year 20. To learn more about the power of compounding interest and investment education go here: https://plushretirement.com/investment-education/

The correct answer would be 5% Compounding Interest, since it is able to add each previous year’s gains to each annual gain. See the graph above. If only a few years then it might still be advantageous to take the higher interest rate, but the longer time span, the greater the compounding effect and even 4% compounding interest outpaces 6% simple interest at year 20. To learn more about the power of compounding interest and investment education go here: https://plushretirement.com/investment-education/

Simple Interest: Interest calculated only on the initial principal amount, without considering any interest previously earned. The formula is Simple Interest = 𝑃 × 𝑟 × 𝑡, where P is the principal, r is the rate, and t is the time.

Compound Interest: Interest calculated on the initial principal and also on the accumulated interest from previous periods. The formula is Compound Interest=𝑃 × (1+𝑟/𝑛) 𝑛𝑡 , where P is the principal, r is the rate, n is the number of times interest is compounded per period, and t is the time.

Simple Interest: Interest calculated only on the initial principal amount, without considering any interest previously earned. The formula is Simple Interest = 𝑃 × 𝑟 × 𝑡, where P is the principal, r is the rate, and t is the time.

Compound Interest: Interest calculated on the initial principal and also on the accumulated interest from previous periods. The formula is Compound Interest=𝑃 × (1+𝑟/𝑛) 𝑛𝑡 , where P is the principal, r is the rate, n is the number of times interest is compounded per period, and t is the time.

The correct answer would be 6% Simple Interest, then 5% compounding interest. The lower compounding rate can’t add enough of the previous year’s gains to each annual gain in under five years. See the graph above. But, after year 8 the smaller compounding interest starts to outpace the simple interest rate. If only a few years then it’s still advantageous to take the higher interest rate whether simple or compounding, but the longer time span, the greater the compounding effect and even 4% compounding interest outpaces 6% simple interest at year 20. To learn more about the power of compounding interest and investment education go here: https://plushretirement.com/investment-education/

The correct answer would be 6% Simple Interest, then 5% compounding interest. The lower compounding rate can’t add enough of the previous year’s gains to each annual gain in under five years. See the graph above. But, after year 8 the smaller compounding interest starts to outpace the simple interest rate. If only a few years then it’s still advantageous to take the higher interest rate whether simple or compounding, but the longer time span, the greater the compounding effect and even 4% compounding interest outpaces 6% simple interest at year 20. To learn more about the power of compounding interest and investment education go here: https://plushretirement.com/investment-education/